Initial 2022 economic data includes further signs of labor market tightness and Fed comments implying a faster removal of accommodation (i.e., rate hikes earlier than anticipated) to combat inflationary pressures. Along with challenges related to the Omicron variant, this has created a bit of a risk-off mentality across markets.

At the margin, the Fed hiking rates faster than expected should impact borrowing rates and spending in 2022, affecting numerous industries including commercial real estate (CRE).

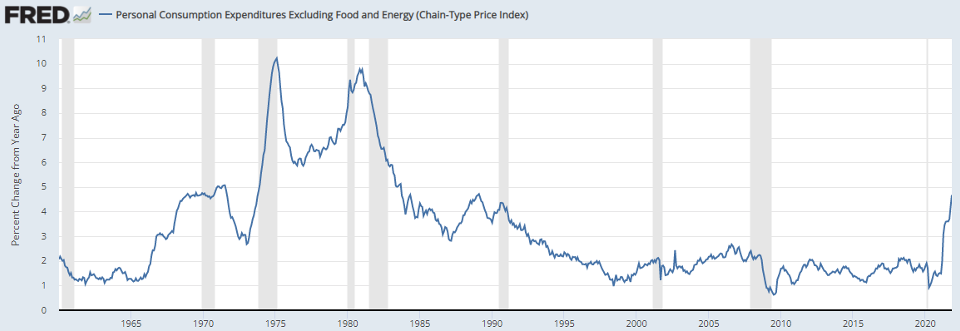

The data argues that the Fed is correct in speeding up the pace of tightening regarding inflationary pressures. Inflation is posting its strongest numbers since the 1980s, driven recently by stimulus spending, supply chain issues, and wage pressures. The following chart shows the Fed’s preferred inflation gauge; Core PCE (Year on Year):

The last time inflation was in this range, the Fed Funds Rate was well above 5%.Today, the Fed Funds Rate is basically 0% arguably way too accommodative given the current tight labor market.

While many continue to debate how long inflation will remain elevated, factors driving price pressures vary in terms of how long they will last. Stimulus-related inflation pressures appear to be waning as financial support measures like enhanced unemployment benefits are no longer being provided. Supply chain inflation pressures remain but should slow down somewhat over the medium term if spending normalizes or slows from less available stimulus and/or rate hikes. The factor that continues to look like a longer-term issue is rising wages from a lack of available labor.

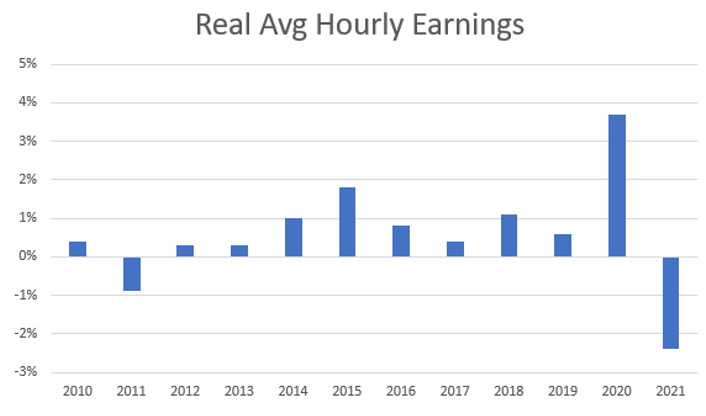

All else equal, rising wages aren’t a ‘bad’ economic outcome, but if inflation growth outpaces wage growth, employees are still worse off as purchasing power suffers. That’s precisely what happened in 2021. Despite wages rising significantly, purchasing power actually fell. As shown in December’s BLS report, real earnings (wages adjusted for inflation) finished 2021 at -2.4%:

The Fed is right to create more restrictive policy. Spending will likely slow, lowering the rate of growth for prices and improving purchasing power for many.

While hiking rates and slowing spending can help the economy stabilize over the medium and long term, it will have a negative impact on many businesses in the short term. Rising borrowing costs, weaker spending, and still elevated wage growth do not create the best environment for CRE investors or users of space. Add in the evolution of remote capabilities and ongoing pandemic fears, and the current environment for many CRE property types (i.e., office, retail, hotel) continues to look murky at best.