The challenge of operating amongst rising input costs is a common theme with our clients in 2021. One of these costs, wage growth, has received plenty of attention this year given the lack of available labor across the U.S. workforce. Job openings sit at historic highs (11 million openings), the unemployment rate is back down to a low rate of 4.2%, and the labor force participation rate remains well below its pre-pandemic level, showing little improvement over the past year.

Employers have been increasing wages to attract and retain talent, creating a challenge for business owners but a seemingly positive outcome for job seekers. Unfortunately, a deeper dive into wage data shows a much less attractive situation for many employees.

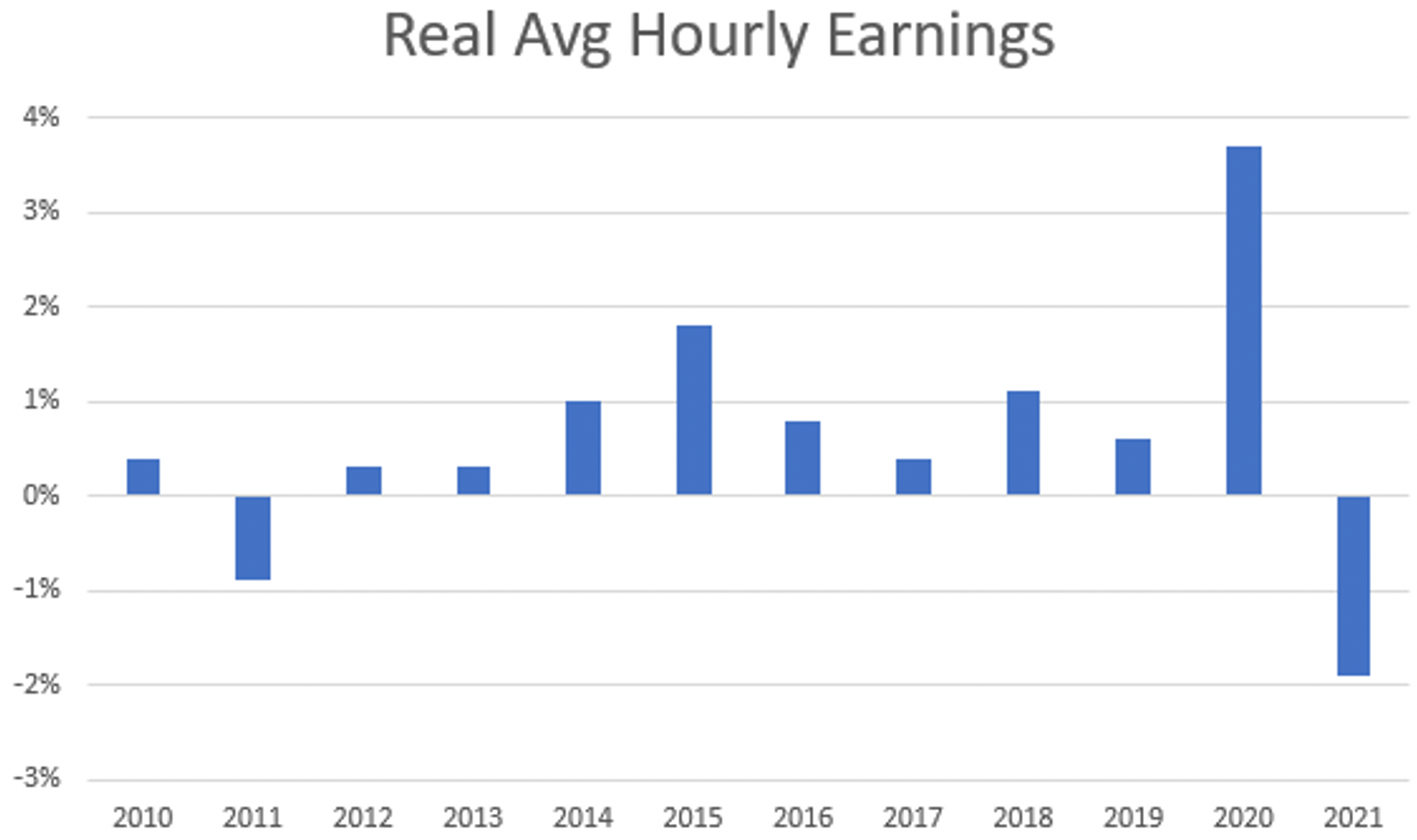

The rising prices of goods and services have outmatched rising wages thus far in 2021, so real wages (wages adjusted for inflation) have actually decreased. Through November, real wages are down 1.9%, the most significant drop for a calendar year since before the Global Financial Crisis:

Charts like the one above are why the Fed is becoming so concerned with inflation. Despite wages rising at their fastest rates in years, wage earners in 2021 made less money relative to the costs of goods and services.

The Fed will likely raise rates more than once in 2022 to slow these inflationary pressures. With the economic recovery mainly supported by stimulus over the past 18 months, the big concern for many is how spending and the recovery will perform with the Fed removing these stimulus measures.

If the Fed hikes, and spending and the recovery falter, what does this mean for commercial real estate (“CRE”) activity, particularly CRE investors, landlords, and users of space? Do office space users downsize due to a combination of revenue lost from less spending and growth of cheaper remote capabilities? Does CRE investment slow down due to rising borrowing costs with the Fed raising rates? These are just a few questions I have as the Fed prepares to take the training wheels for the recovery in 2022. It will be interesting to see how markets, regions, and industries like CRE react and respond.